Week ended Jan 28, 2023, interesting news items to look at this week were:

1. Huge Margin Call on the Anglo American Empire and NATO: War is a game with no rules because your adversary always try to frustrate whatever plans you may have. Wars on a global scale happen only at intervals of around 80 years because with a global conflict also comes a change in the global world order. It takes very wise emerging leaders to avoid, prepare and then win global conflicts but very foolish sitting world powers, driven by fear, will hastily start wars and loose. The reason, an emerging power has less resources and must meticulously calculate the odds and weigh the possible outcome of every battle. The reverse applies for a sitting power because of over confidence that comes with a lifestyle of abundance. Chapter 1 Verse 26 Sun Tze Art of War. (Fig. 1)

Putin defines victory in a war as “the political objectives for that war has been accomplished”. Bush declared “Mission Accomplished” for the war in Iraq on May 1, 2003 but US was still fighting ISIS in Iraq during the Trump years and had not been for Putin’s intervention and victory in Syria, Biden would still be fighting in Iraq. (Fig. 2).

This week the media is obsessed with news of tanks to Ukraine but to an astute student of warfare, all the signs of NATO falling to disintegration this summer are there already. The facts are straight forward but first let us examine a few strategic moves of Russia and the Anglo American Empire over the past 11 months:

(i) First Iteration of Conflict: ACTION: The AFU(NATO) used 8 years to build an army, hiding behind the deceptive Minsk Accord, to attack the Donbass with the hope of repeating what NATO did to the disarmed Serbian “protection areas” in the Krajinas (operation Storm). REACTION: The RAF preempted NATO’s attack, but not by directly attacking the AFU in the Donbass, but by basically destroying all the AFU military assets in the entire Ukraine. CONCLUSION: the Ukrainian military was pretty much destroyed in the first month of the war.

ACTION: the Anglo American Empire seized Russia’s financial assets and weaponized SWIFT in an attempt to bring down the Russian economy. REACTION: Russia weaponized energy supplies and in one fell swoop destabilized the Western financial and economic structure. CONCLUSION: Very high inflation in the Western alliance but very close co-operation in the Global South and OPEC +. Sanctions by the West became isolation of the West.

(ii) Second Iteration of Conflict: ACTION: The RAF sent to Ukraine a limited land force to multiple locations to shape the battle fields leaving the AFU basically fixed in locations where they were before the SMO. This fragmented the entire AFU. REACTION: NATO send all of the former Warsaw Treaty Pact (“WTP”) equipment from all the former WTP countries to the Ukraine. Send more Ukrainian soldiers to the frontlines at Donbass. CONCLUSION: For fear of air strikes in the open fields, the AFU dared not leave their fortified locations.

ACTION: The RAF avoided the AFU elite forces at Bakmut (60% of AFU fighting force) but instead took out the Ukranonazis at Mariupol and also the Ukraine Southern Regions. REACTION: AFU dared not leave their fortified locations to reinforce the Azov Brigade in Mariupol and the Southern Regions. Mariupol was taken with the majority of the Ukrainonazis fighting force destroyed. (Fig. 3)

The entire NATO C4ISR capabilities were gradually made available to the AFU which seriously complicated Russian operations while greatly aiding the Ukrainian artillery and air force. CONCLUSION: The RAF has to beef up significantly boots on the ground in Ukraine to fight NATO. Putin legally enabled 4 Oblast in Ukraine to cede from Ukraine and ascension into the Russian Federation. (Author’s Note: This RAF strategy of attacking Azov first was used by Mao in his “long march” and called “圍点打援- wei dian da yuan”. Literally meaning encircle a strategic point to draw and attack the adversary reinforcement in the open. Please read on previous Report dated March 2, 2022)

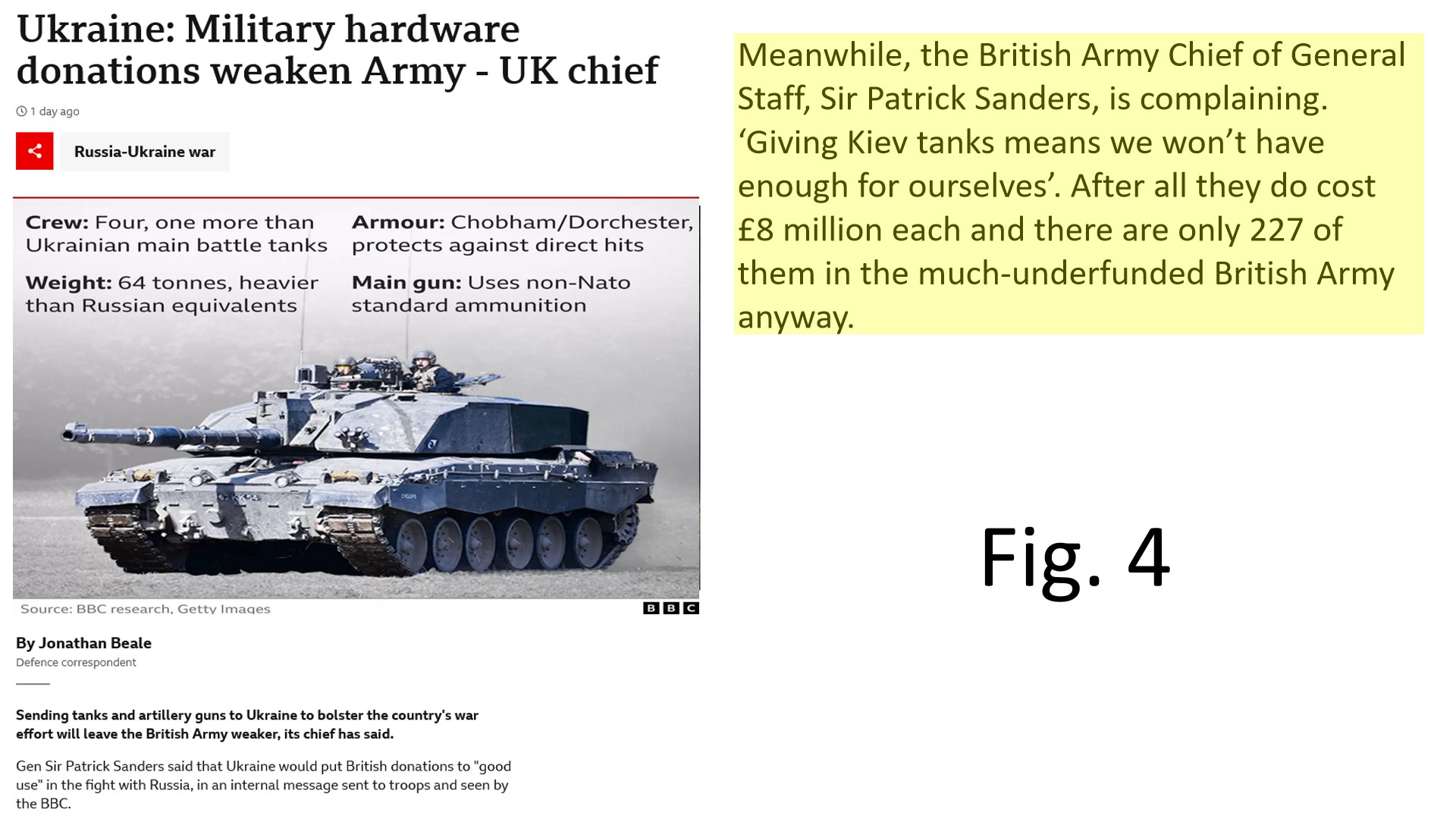

(iii) Third Iteration of Conflict: ACTION: the AFU counter a major offense at Kherson and RAF orderly withdrew. AFU lost a lot of hardware and soldiers but RAF kept casualties to a minimum. AFU liberated Kherson city. At the third iteration, the casualties of AFU to RAF was 10:1 because the comparative fire power of AFU to RAF was 1:10. REACTION: RAF reorganized and moved against the elite forces at Bakmut, the entire Donbass became one huge cauldron, open only on the western side. This is a repeat of “圍点打援- wei dian da yuan”. Kiev vowed to hold Bakmut and sent in as much reinforcements as can be spared. Estimated AFU KIA/MIA is now over 150,000 and adding in the wounded, the number of AFU soldiers incapacitated is now well over 500,000. From Telegraph private citizen’s Video Channels, Ukraine police is now conscripting men between 12 to 60 to put them in uniform and thrown to the front line. Ruslan Borysovych Khomchak, Commander-in-Chief of Ukraine Armed Force, wants 300 tanks and 600 infantry armored vehicles, as well as 500 Howitzers by August 2023 or else it, said General Borysovych will be too late. CONCLUSION: For weeks, we have reported the Anglo American Empire and her cronies have exhausted their ability to produce and to give what Ukraine needed. From (Fig. 4) you will see the promised number of tanks to be made available to Ukraine will be less than half as demanded, in substance, only 15% (46 tanks) may actually be deployed in Ukraine by mid July 2023. Getting these tanks from the border to the front line posses another problem.

Of the required 500 Howitzers, none is included in Washington latest $2.5 billion military aid package. By comparison, Russia is producing 20 to 40 brand new modern T-90 tanks a month. In overall context, as of Jan 14, 2023 RAF has destroyed 7500 armoured fighting vehicles of all types in Ukraine. (Fig. 5).

So how much difference will it make for an additional 46 to 140 tanks staggered to be delivered in months if not by years.

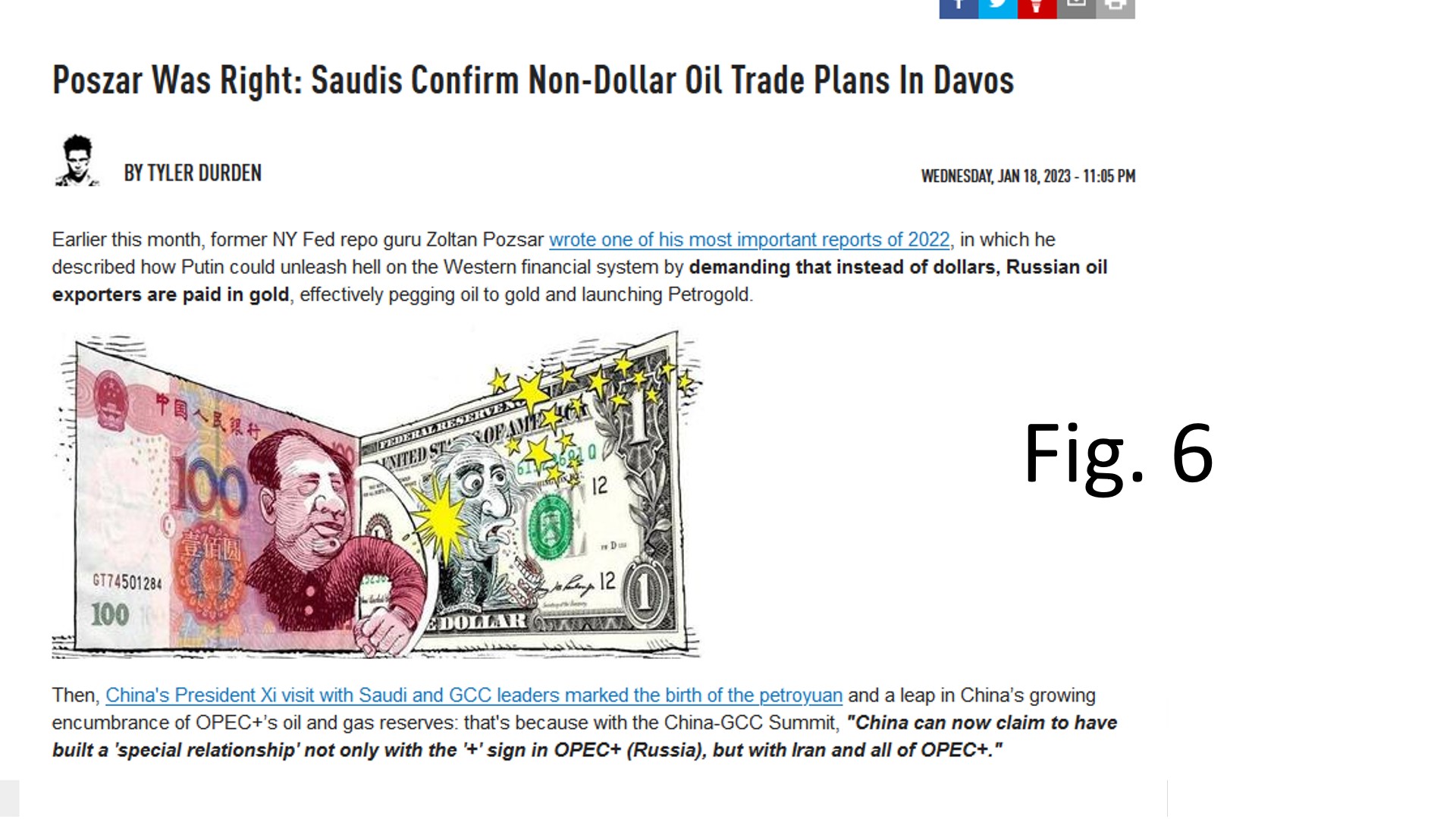

In my usual financial lingo, a huge margin call is made against the Anglo American Empire and NATO and they are unable to meet the call. Ukraine will finish and with it, NATO will disintegrate. Just watch one by one, rats will jump off this sinking ship and immoral politicians have already begun raiding the Treasury. (Fig. 6)

Caution! just make sure you are not the one that is left holding the USD bag.

2. Two US Military Studies of Interests published in Jan 2023: If you are still skeptical after reading the preceding paragraphs, please continue to read two recent war game studies by respectively CSIS and the Rand Corporation.

(i) The first report titled “The First Battle of The Next War”: The study modeled a war between US and China in defence of Taiwan. It concluded US would be successful assuming China only exercised a naval blockade against Taiwan and Taiwan could withstand a Chinese amphibian landing until the US arrives in full strength. The war game assumptions of course ignore China has the capability of sinking all US Aircraft carrier simultaneously using her full range of hyper-sonic missiles. But read between the lines in the report: The US used up its inventory of LRMs (Long-Range Missiles). JASSMs (Joint Air-to-Surface Standoff Missile), LRASMs (Long Range Anti-ship Missiles), Harpoons (Anti-ship missile), TLAM (Tomahawk land-attack missiles) in the first week in every iteration of the modeled conflict, CSIS noted, adding that the weapon’s production time is two years.(Fig. 7)

(i) The second report titled “Avoiding a Long War” by the Rand Corporation on a study of US involvement in the Russia/Ukraine conflict . The conclusion:” In short the consequences of a long war - ranging from persistent elevated escalation risk to economic damage - far outweigh the possible benefits”. The Reason: According to the authors, the conflict has already inflicted significant economic, military and reputational damage on Russia, so its “further incremental weakening is arguably no longer as significant a benefit for US interests.” The price to the West has not been insignificant either, from the disruption to energy, food and fertilizer markets to the cost of “keeping the Ukrainian state economically solvent,” which will only “multiply over time.” (Fig. 8).

Someone has finally worked out in these loose loose game, every war participant will turn out to be a looser, including USS Amerika.

For those interested in reading the above full reports, the links are listed below:

https://www.naval.com.br/blog/wp-content/uploads/2023/01/Wargaming-a-chinese-invasion-of-Taiwan.pdf

https://www.rand.org/pubs/perspectives/PEA2510-1.html

3. De-dollarization, one more puzzle in place: Brazil and Argentina nerve themselves up to make Latin America sovereign region (Fig. 9).

Discussions are in place for indigenous currencies to be employed for regional trading in South America in place of USD.

This week financial markets results as follows:

A. Stock Market: For the week ended Jan 28 2023 Dow gained 602.5 points (+1.8%). (Fig. 10)

As reported last week, Fed’s Open Mouth Policy has but limited short term effect. As consumer spending continued to weaken and Big Tech announced layoffs in sequence, a classic short squeeze occurred and stock short sellers capitulated and covered their shorts. The market gave the middle finger to the Fed Hawks.

B. Debt Market: (Fig. 11): USGG10YR ended the week at 3.507% a gain of 8.7 basis points from the previous week.

The effects of Fed’s Open Mouth Policy waned and stocks were bought, bonds were dumped within a trading range. Spread between USGG2YR and Fed Funds continued to stay negative expressing the financial market did not favour nor believe justified large rate hikes again. (Fig. 12).

Very short term bill and long 30 Bond rates dropped slightly while term Treasury Notes rates rose by 4 to 7 basis points. The already severely inverted UST Yield Curve continued a steep inversion making bank credits to main street impossible and a severe recession is written in and banking crisis imminent.(Fig. 13).

The US Federal Govt has reached its debt ceiling and the tight credit market begins to affect Money Supply Growth (Fig. 14).

Domestic Reverse Repo has slowed as Treasury stopped borrowing and the need for window dressing disappeared. However Foreign Reverse Repo continued to spike because real foreign holders mercilessly dumped US Treasuries and the need for window dressing by cronies of the Anglo American Empire became a 24/7 routine. (Fig. 15).

As of 25th January 2023, weekly losses at the Federal Reserve has snowed ball to $25.8 billion. By conventional standard of accounting, the Federal Reserve is bankrupt and so is BOE, ECB and BOJ. (Fig. 16).

As an emergency measure, US Treasury has stopped contribution into the Pension, Retirement and Social Security Accounts and cash resources of US Treasury as of Jan 25th 2023 stood at $491.8 billion. (Fig. 17).

Janet Yellen said the Federal Govt can last until June 2023 but I suspect the crunch would come much sooner and thereafter QE to infinity and hyper-inflation.

C. FX Market (Fig. 18): for the week ended Jan 28, 2023, DXY opened at 101.992 and closed at 101.922 (Down -0.07%).

FX traded at a narrow range with Rmb steady against USD whilst Yen gathered strength against USD, GBP and EUR.

Oil eased 3% on account of weak economic data while precious metals were steady (Fig. 19)

D. Precious Metals & Crypto :(Fig. 20): Gold price opened at $1925.3, and closed the week at $1927.29 (+$1.99, +0.1%).

Silver lagged gold and showed price decline of 1.3% . The diversion between gold and silver was basically a case with Investment funds adding to their long god position whilst hedge funds shorted silver. Bitcoin followed the stock market rebound and further gained 3.5%.(Fig. 21)

Luke 12:15 And He said to them, "Take heed and beware of covetousness, for one's life does not consist in the abundance of the things he possesses." 16 Then He spoke a parable to them, saying: "The ground of a certain rich man yielded plentifully. 17 And he thought within himself, saying, 'What shall I do, since I have no room to store my crops?' 18 So he said, 'I will do this: I will pull down my barns and build greater, and there I will store all my crops and my goods. 19 And I will say to my soul, "Soul, you have many goods laid up for many years; take your ease; eat, drink, and be merry." ' 20 But God said to him, 'Fool! This night your soul will be required of you; then whose will those things be which you have provided?' 21 "So is he who lays up treasure for himself, and is not rich toward God."