Week ended Jan 21, 2023, interesting news items to look at this week were:

1. Unfanged: Recurrent news continued to surface on critical supply problems facing the Anglo American Empire (Fig. 1):

(i) Demilitarized NATO: One of the stated objectives of Putin’s Special Military Operation in Ukraine is to demilitarize Ukraine. But as Ukraine Defense Minister self admitted that Ukraine was but carrying out NATO’s mission, a demilitarized Ukraine would also mean a demilitarized NATO. (Fig. 2) Fox News reported this week “the US is looking under every rock for munitions”.

Separately, NY Times reported “With stockpiles in the United States strained and American arms makers not yet able to keep up with the pace of Ukraine’s battlefield operations, the Pentagon has turned to two alternative supplies of shells to bridge the gap: one in South Korea and the one in Israel,”(Fig. 3).

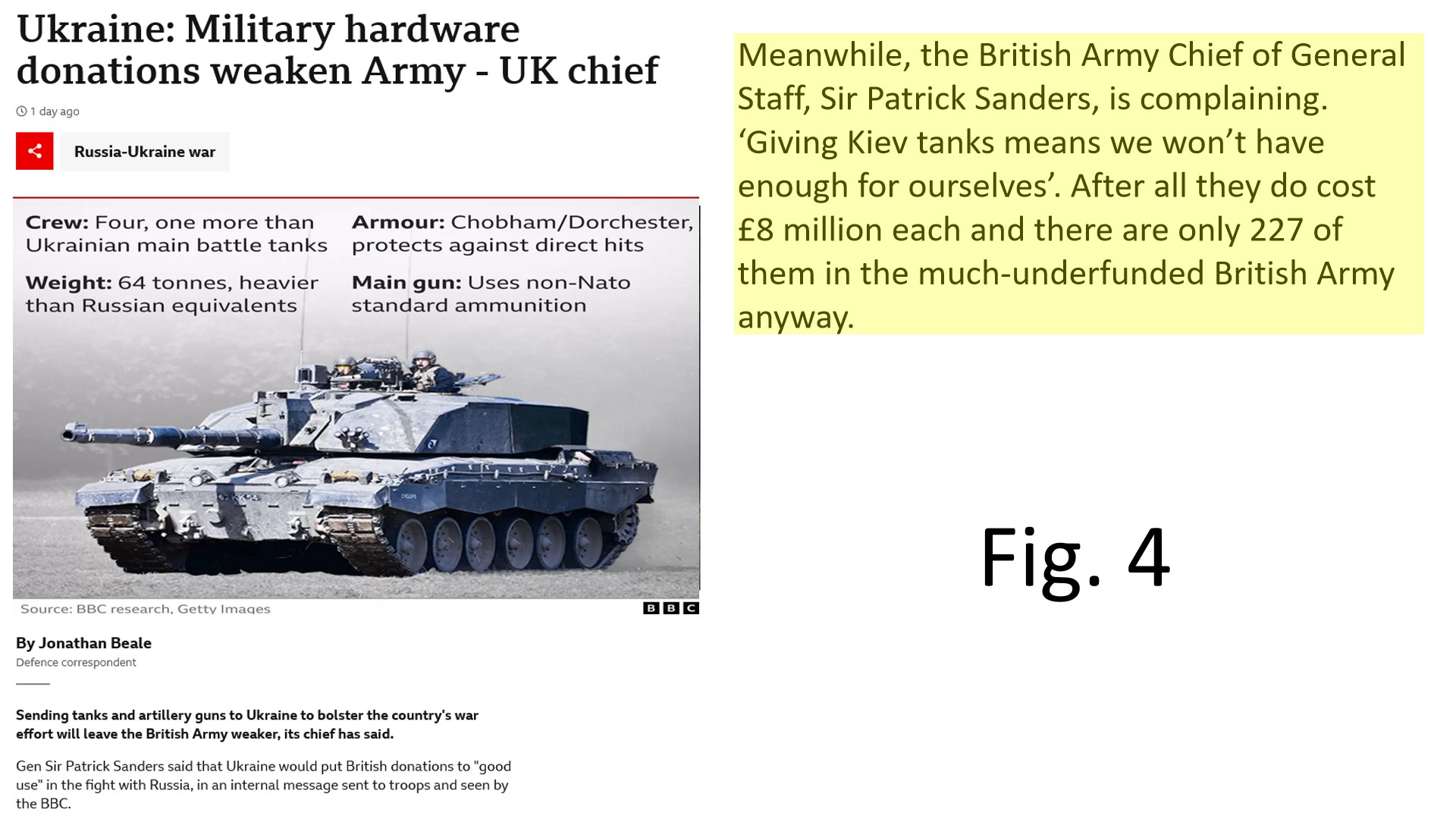

BBC echoed “Meanwhile, the British Army Chief of General Staff, Sir Patrick Sanders, is complaining. ‘Giving Kiev tanks means we won’t have enough for ourselves’. After all they do cost £8 million each and there are only 227 of them in the much-underfunded British Army anyway.(Fig. 4).

The foregoing were not random reporting, The Centre for Strategic and International Studies (“CSIS”, an American bipartisan pro-war think tank) published on January 9 2023 a study called “Rebuilding U.S. Inventories: Six Critical Systems” calculated (Fig. 5)

much of what was given to Ukraine could not by replaced within the next 5 years. Specifically, the current US annual production rate for 155mm munitions for Howitzer M777 would be totally spent by Ukraine in just 15 days. It appears on the other hand Russia’s industrial capacity is allowing real time restocking of munitions employed in the SMO.

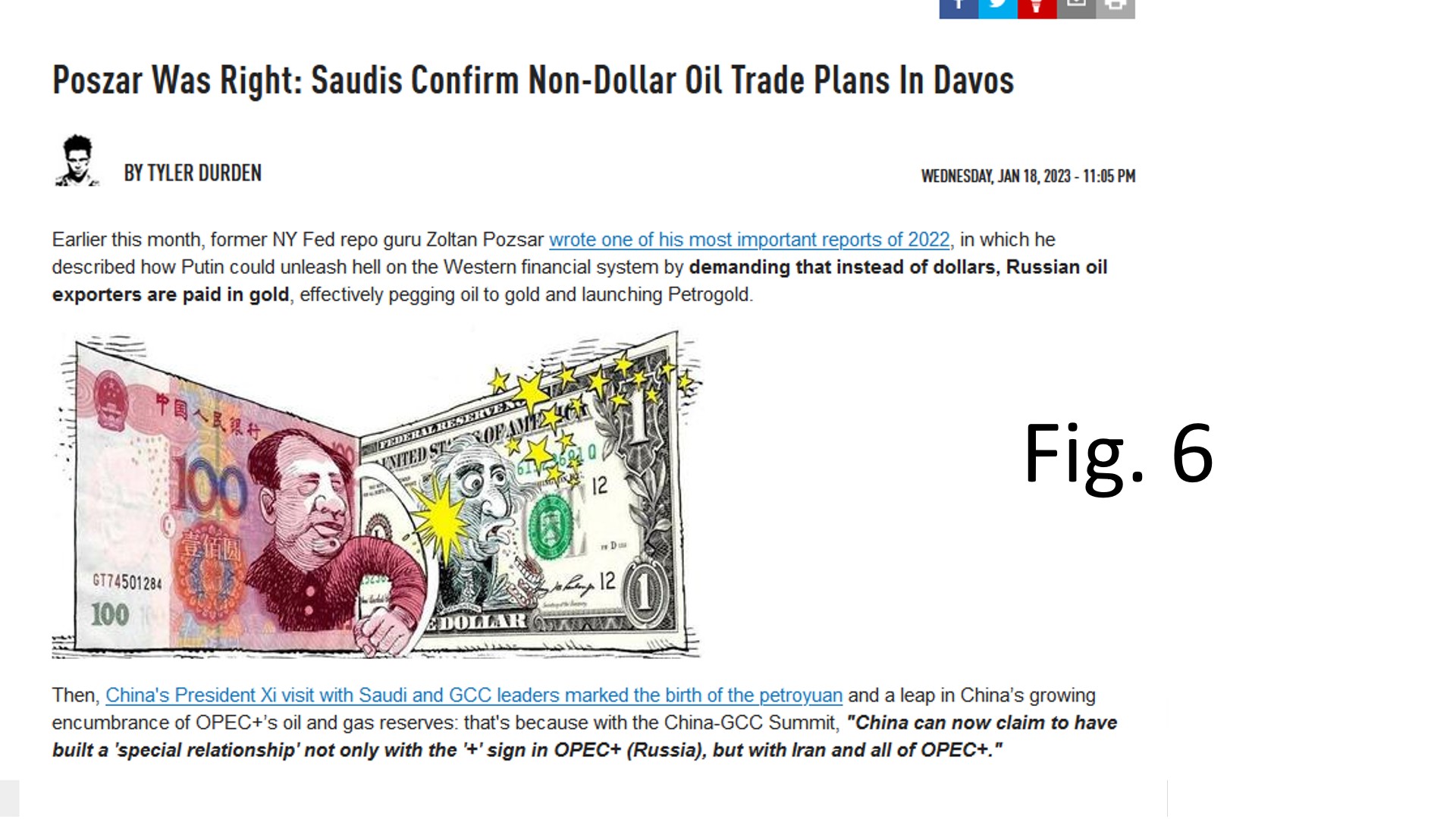

(ii) Global De-dollarization: At the Davos WEF Conference this week, the Saudis officially confirms its Non Dollar Oil Trade Plans. (Fig. 6).

Figures published by US Treasury this week in her International Capital Flow report (TIC) reinforced the mega trend of de-dollarization as Central Banks and Official Agencies dumped $509.8 billions of US Treasuries cumulative to November 2022 calender year. (Fig. 7).

Strangely for the first time, US Treasury backtracked and revised all historical reported numbers on flow balances but did not explain why. This puts comparison and analysis more difficult. Such tactics smells.

When two of the final pillars of strength of the Anglo American Empire begins to look shaky (the US military and the dollar hegemony) you know they are pushed close to the precipice. We pray for sanity as WWIII means nothing short of a nuclear holocaust.

2. Civil Unrest Cycle: Rolling strikes by multiple workers unions in the UK for higher pay and one million combined strike in France against extending pensionable age marked the season for the Civil Unrest Cycle for 2023. (Fig. 8)

3. The Western Alliance is not all smelling roses: 25 Years ago, the French Ministry of Armed Fores set up École de guerre économique (EGE, The School for Economic Warfare). A recent survey of French Nationals public by EGE when asked “Economic War: Who is the Enemy?” puts US ahead of China and Germany ahead of Russia. (Fig. 9).

No wonder commentators now reduced the principal adversaries against Russia down to US-UK-Poland-Ukraine. We wait and see if the MSM poisoning of the collective Western minds against the East is actually weaning off.

This week financial markets results as follows:

A. Stock Market: For the week ended Jan 21 2023 Dow dropped 927.12 points (-2.7%) nearly wiping out all the gains of the previous two weeks . (Fig. 10).

In a repeat of almost identical Fed Open Mouth Policy two weeks ago Jim Bullard (St. Louis Fed President, but a non voter this year) spooked the financial market again with hawkish restrictive policy talk (Fig. 11).

Like the US Military Armory, the Fed is running out of ammo and have to rely on talking to cool inflation expectation. Of course the financial market by itself would not have reacted so strongly without behind the scene market manipulations, particularly the highly leveraged, HFT algo derivatives driven CTA funds. Give it 2 to 3 weeks, it will unwind by itself. In the meantime, the dog fight between the Red Elephant and the Blue Donkey may mean the US Treasury might be out of cash by second week of February. (Fig. 12).

Current cash balance of US Treasury stood at $377.5 billion and average weekly expenses is $110 billion. (Fig. 13)

B. Debt Market: (Fig. 14): USGG10YR ended the week at 3.482% a drop of 1.6 basis points from the previous week, hardly affected by the Fed Speak.

Spread between USGG2YR and Fed Funds have gone further negative expressing market did not favour nor believe justified large rate hikes again. (Fig. 15).

The already severely inverted UST Yield Curve further sloped down to longer dates making bank credits to main street impossible and a severe recession is written in and banking crisis imminent.(Fig. 16).

In fact, The St. Louis Fed has quietly published data indicating that the US is now entering a recession. This admission was posted right before the new year on Dec 28, clearly as a means to avoid wider media attention. The news also comes not long after the Philadelphia Fed revised their 2nd Quarter labor growth numbers, erasing a whopping 1 million jobs from their original estimates. (Fig. 17)

C. FX Market (Fig. 18): for the week ended Jan 21, 2023, DXY opened at 102.180 and closed at 101.992 (Down -0.18%).

Major events in FX market this week was BOJ further backtracking on Yield Curve Control (YCC through widening of managed tolerance of JGB) and BOE raising interest rate by 50 basis points. As a result GBP up and JPY down by 1.35% respectively. CNY is Asia followed JPY was also down 1.2% but Euro was steady. Following BOE rate decisions, oil and precious metals were slammed down in London as bullion bankers tried to wash and rinse out weak long positions but oil and gold rebounded quickly. Only silver prices lagged. (Fig. 19)

D. Precious Metals & Crypto :(Fig. 20): Gold price opened at $1919.4, and closed the week at $1925.3 (+$5.9, +0.3%),

early in the week Hedge Funds added back their long position in silver but Bullion Banks took advantage of BOE rate increase to slammed silver prices down with silver price down b 1.4% for the week. The whales of Bitcoin is setting up another bear trap and Bitcoin price powered ahead by another 12.65%, cumulative to a 30% rise in 2 weeks against a flat stock market. Let’s see who the whales will have lunch later on. (Fig. 21)

Proverbs 15:16 Better is a little with the fear of the LORD, Than great treasure with trouble. 17 Better is a dinner of herbs where love is, Than a fatted calf with hatred. 18 A wrathful man stirs up strife, But he who is slow to anger allays contention. 19 The way of the lazy man is like a hedge of thorns, But the way of the upright is a highway.

No comments:

Post a Comment